What Every Home Owner Should Know About Mortgages

Article writer-Moos McGrawMortgages are used to finance a new home purchase. It is also possible to obtain a second mortgage for a home you currently own. The advice in this article can help you get a great rate, no matter what mortgage type you are interested in.

Having the correct documentation is important before applying for a home mortgage. Before speaking to a lender, you'll want to have bank statements, income tax returns and W-2s, and at least your last two paycheck stubs. If you can, prepare these documents in electronic format for easy and quick transmission to the lender.

You should have a work history that shows how long you've been working if you wish to get a home mortgage. Most lenders require a solid two year work history in order to be approved. An unstable work history makes you look less responsible. Also, never quit a job while applying for a loan.

Really think about the amount of house that you can really afford. Banks will give you pre-approved home mortgages if you'd like, but there may be other considerations that the bank isn't thinking of. Do you have future education needs? Are there upcoming travel expenses? Consider these when looking at your total mortgage.

Do your research before you go to a mortgage lenders. Having all your information available can make the process shorter. Your lender will need to see this necessary information, and having it on hand will help speed up the process.

If your mortgage has been approved, avoid any moves that may change your credit rating. Your lender may run a second credit check before the closing and any suspicious activity may affect your interest rate. Don't close credit card accounts or take out any additional loans. Pay every bill on time.

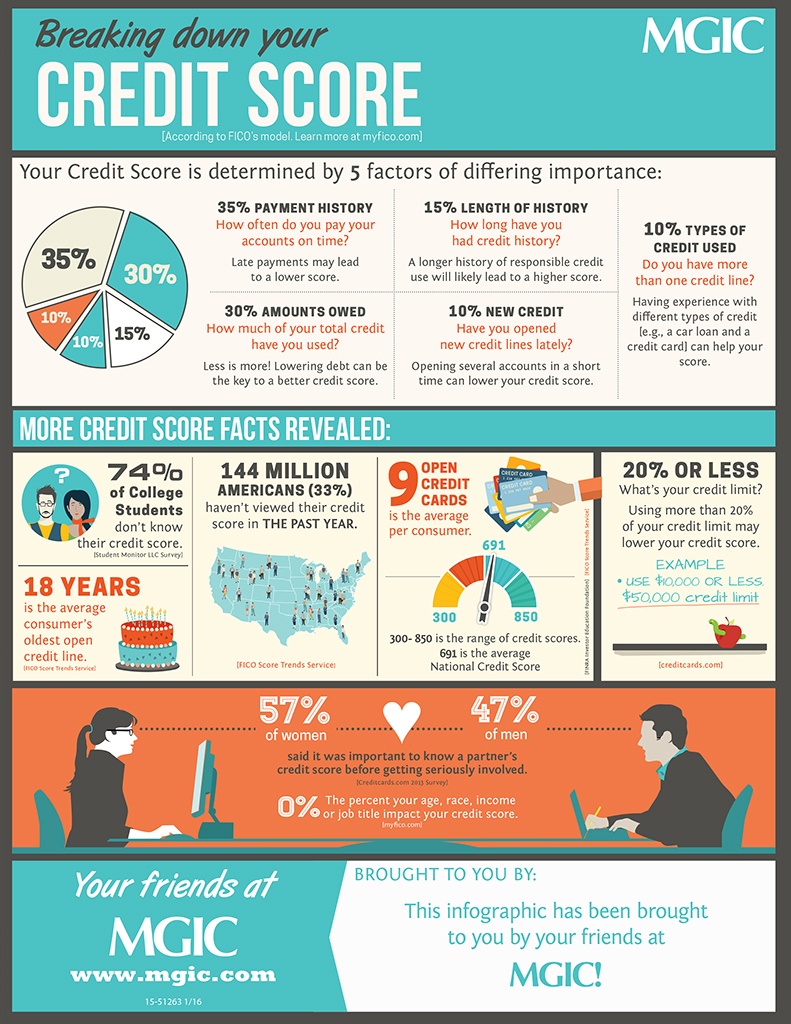

Educate yourself about the tax history of any prospective property. Before putting your name on documents for a mortgage, it is crucial to know what property taxes will cost. If the tax assessor puts a higher value on your property than you know of, you will have a surprise coming.

Before you apply for a mortgage, know what you can realistically afford in terms of monthly payments. Don't assume any future rises in income; instead focus on what you can afford now. Also factor in homeowner's insurance and any neighborhood association fees that might be applicable to your budget.

Know how much you will be required to pay in fees prior to signing any agreement for the mortgage. You will be required to pay closing costs, commission fees and other charges. These can possibly be negotiated with the mortgage lender or seller.

Mortgage rates change frequently, so familiarize yourself with the current rates. You will also want to know what the mortgage rates have been in the recent past. If mortgage rates are rising, you may want to get a loan now rather than later. If the rates are falling, you may decide to wait another month or so before getting your loan.

Never assume that a good faith estimate is fact or written in stone. It is in fact not just an estimate, but one written in good faith. Always be wary of extra costs and fees that can creep into the official and formal paperwork later that drive up your total expense.

Do not even bother with looking at houses before you have applied for a home mortgage. When you have pre-approval, you know how much money you have to work with. Additionally, pre-approval means you do not have to rush. You can take your time looking at homes knowing that you have money in your pocket.

When looking for a mortgage, compare the offers available from several brokers. A low interest rate is one major consideration. You should also consider the different types of loans that are being offered. You need to know about down payments, the closing cost and any other fees associated with the loan.

Get at least three mortgage offers before deciding on which one to go with. Home mortgages, like many other loans, will vary in their costs and rates from lender to lender. What you think is a good deal may not be, so it's important to see multiple options before making a decision.

Think about applying for a home mortgage where you make your payments just two weeks apart. Doing this allows you to make two extra payments each year, which can greatly reduce the amount that you pay in interest over the term of the loan. It's also ideal if you're getting income every other week so that you can just get the payment taken from your bank.

Make sure you've got all of your paperwork in order before visiting your mortgage lender's office for your appointment. While logic would indicate that all you really need is proof of identification and income, they actually want to see everything pertaining to your finances going back for some time. Each lender is different, so ask in advance and be well prepared.

Before you agree to a mortgage commitment, ask for a written description of any fees and charges. There will be closing costs, which should be itemized, and other miscellaneous charges and commission fees. You may be able to negotiate some of the fees.

If your downpayment is less than 20% of the sales price of the home you want to buy, expect the mortgage lender to require mortgage insurance. This insurance protects the lender in the event that you can't pay your mortgage payments. Avoid mortgage insurance premiums by making a downpayment of at least 20%.

There are times when the seller of a home will be able to give you a land contract so you can purchase the home. The seller needs to own the home outright, or owe very little on it for this to work. A land contract may need to be paid within a few years.

Using the things you've gone over here is going to help you when making a decision about a mortgage. There are tons of resources available and you don't have to let your mortgage be a disappointment. Let the information you learn guide you towards making a great decision.